Even my cat is reading Rich Dad Poor Dad!!!

Even my cat knows we need to get our global financial purses in order.

Now it seems funny. Heck it is.

However the sad truth is not enough people are focused on their financial education. Even fewer people are focused on their financial well being. The average American is simply following what their payroll secretary instructs them to do. No offense to the payroll secretaries of the world but they are not financial advisers. They do not have to be. It isn’t a requirement. And in fact in many ways they don’t have your best interest at heart. They may round your overtime down per instruction. Hey legal or not that puts them against the dollars you earn when you trade sweat equity for a paycheck. below I’m going to give you my ideas on a few investments, assets, financials you need and or don’t. Ahead of time let me say I am NOT, repeat NOT a financial advisor. I’m just a well read, educated guy from the city that learned the hard way. Feel free to challenge me on redirect- also known as the comment section.

-Investments.

Many people are banking on investments they don’t understand and don’t control to see them through to the end. Regardless of. Lifespan. Sadly after the last crash- the game of economics has changed. I’m not being callous either. Your life isn’t a game but when you let strangers play with your money and wish for the best- you are doing worse than a guy who plays monopoly with his dog. Solution: ask questions. Find out what the fees are. What is your guaranteed ROI aka return on investment. If you can’t understand the product they sell you- Walk away. They get paid to educate you and serve you! Investments don’t have to be stocks and bonds. They can be metals, rental properties, reits, and many more. Look around. Educate Yourself.

-Assets.

Assets build for you essentially. A house you own free and clear is an asset. A sack of junk silver, also known as a bag of coins with no numismatic value and a high amount of silver in them, that’s an asset. A Porsche is not an asset. A cool toy and a burden on your wallet is what a Porsche is.

A rental property with positive cash flow every month is an asset. A home you live in with a mortgage is not an asset in my opinion. If you can lose it or you can’t pay it off in one swipe, then it is a burden. Now people with mega bucks may use a mortgage and a jumbo loan to create certain incentives and complicated fiduciary vehicles to benefit them. I’m not that guy and most of is aren’t either. So skip them lol. In essence an asset puts money in your pocket.

-Liabilities.

Back to the Porsche. Its awesome. I want one. I drive a Honda Accord sedan. You family can and no kids lol. I’m trying to plan ahead. My car is not an asset either. When I leased it however I had a nice tax write off for my home business. See how you can work things? Your home- sorry. Liability like I said before. Mortgage, insurance, maintenance, hoa dues, water bill, electricity- the list goes on. And heaven forbid your boiler or hvac system goes. Got 10 grand sitting around? The play station 3 and surround sound system your kid had to have- pricey liabilities. Oh and the 70 inch Sharp Aquos. Great tv. Li-a-bi-li-ty! Now you need shelter and transportation but evaluate your means and needs. Nothing wrong with having wants too. However find a balance. Don’t be ignorant. Don’t keep up with the jones’. Build your future.

-Physical wealth.

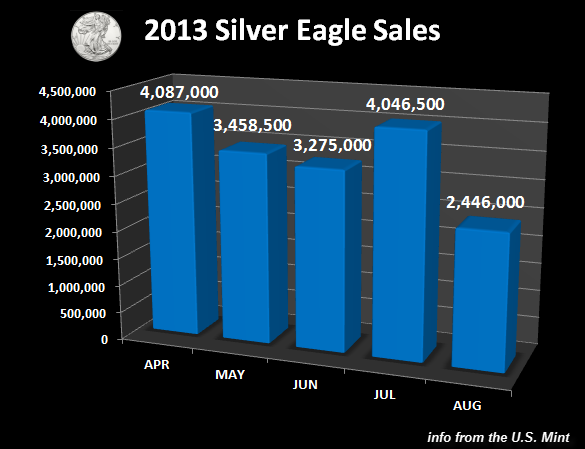

I love physical wealth. Gold, silver, platinum palladium- AMEN! These are my ideas of Assets and Investments. Gold has historically been a way to hedge against inflation and store wealth. Silver as well. Silver coins are highly collectible and can be fun to collect and teach the kids money lessons with. Sealed, signed, graded coins are considered numismatics and can gain value beyond their weight in silver or gold. You can buy junk silver as well. Try this- sort your silver coins for a week. Anything from 1965 or early has a decent chunk of silver in it. A 1960 nickel is 2 bucks. The quarter is 8 bucks. Now of course this all depends on silvers value as adjusted daily, but I assume you see the idea. Questions or want more info on this- reach out to me asap.

-Savings accounts.

Both are good. You should save a portion of every dollar you make until you die. No excuses. No usage. Ask your bank to remove $25 bucks from every check, $10 if you can’t squeeze it out. This way it goes right to savings and you don’t spend by accident. Putting money away for Christmas, or a new car is smart too.

-Emergency fund.

This builds off of the previous. We all need x amount of dollars set aside for life’s hardships. Suze Orman says save six months of living expenses. I concur but that’s a lot of money for all of us. So start with 1000 dollars as your initial goal. You can get there faster than you think.

-Fees.

This is money you can use to build that emergency fund.

checking fees are killing most people. Use direct deposit or get the most basic service you can.

Monthly installment geico vs 6 months upfront. This will save you 60 dollars a year. If you make the payments upfront you skip the fees. Life insurance does the same and so do many other payments. Mortgage and car- send am extra 100 bucks a month to- THE PRINCIPAL. This will reduce interest and fees. It will also add about a payment a year. Lastly this kind of math will take years off your mortgage and months or years off your car loan. Think folks.

Lastly- you don’t need the Cable gold package. You want it. Get the basic. Heck, get Netflix and only the internet. That 80 to 100 dollars you save monthly will give you 960 to 1200 dollars a year!

Are you with me yet folks?

There is money in your wallet/purse. You have to want it though. Do you need change? Tired of the boss? Want to get rid of debt. Well I just gave you some concepts and strategies and info you may not have been privy to before. Use it. Grow.

And remember:

You #thriveorsurvive by your own hand.

#thriveorsurvive.

Thoughts? Concerns?

Questions? Think I’m wrong?

Let’s chat.

Need ideas?

Want to learn how to invite?

Let’s chat.

Want a mentor or maybe the guy who will bounce ideas back and forth with you?

Let’s chat-

Tony@Changeinadvance.com

@changeinadvance

http://www.changeinadvance.com

Or simply reply to this article.

Tags: #$, #thriveorsurvive, @changeinadvance, cat, conspiracy of the rich, depression, economics, facts, finance, global conspiracy, mba, money, recession, rich dad poor dad, robert kiyosaki, rules, success